Chapter 2

Thinking Like an Economist

Intro

- What are economists’ two roles? How do they differ?

- What are models? How do economists use them?

- What are the elements of the Circular-Flow Diagram? What concepts does the diagram illustrate?

- How is the Production Possibilities Frontier related to opportunity cost? What other concepts does it illustrate?

- What is the difference between microeconomics and macroeconomics?

- What is the difference between positive and normative statements?

The Economist as a Scientist – 1

- Economists play two roles:

- Scientists: try to explain the world

- Policy advisers: try to improve it

- Scientists: try to explain the world

- As scientists, economists employ the scientific method:

- Dispassionate development and testing of theories

- Devise theories, collect data, and analyze data to verify or refute theories

- Dispassionate development and testing of theories

The Economist as a Scientist – 2

- Scientific method in economics:

- Observation → collect and analyze data

- Develop a theory based on observed data

- More observation → evaluate the theory

- Observation → collect and analyze data

- Cannot use lab experiments → rely on natural experiments offered by history

The Economist as a Scientist – 3

- Economists make assumptions

- Simplify the complex world

- Simplify the complex world

- Economists use models

- Built with assumptions

- Omit many details → focus on essentials

- All models are subject to revision

- Built with assumptions

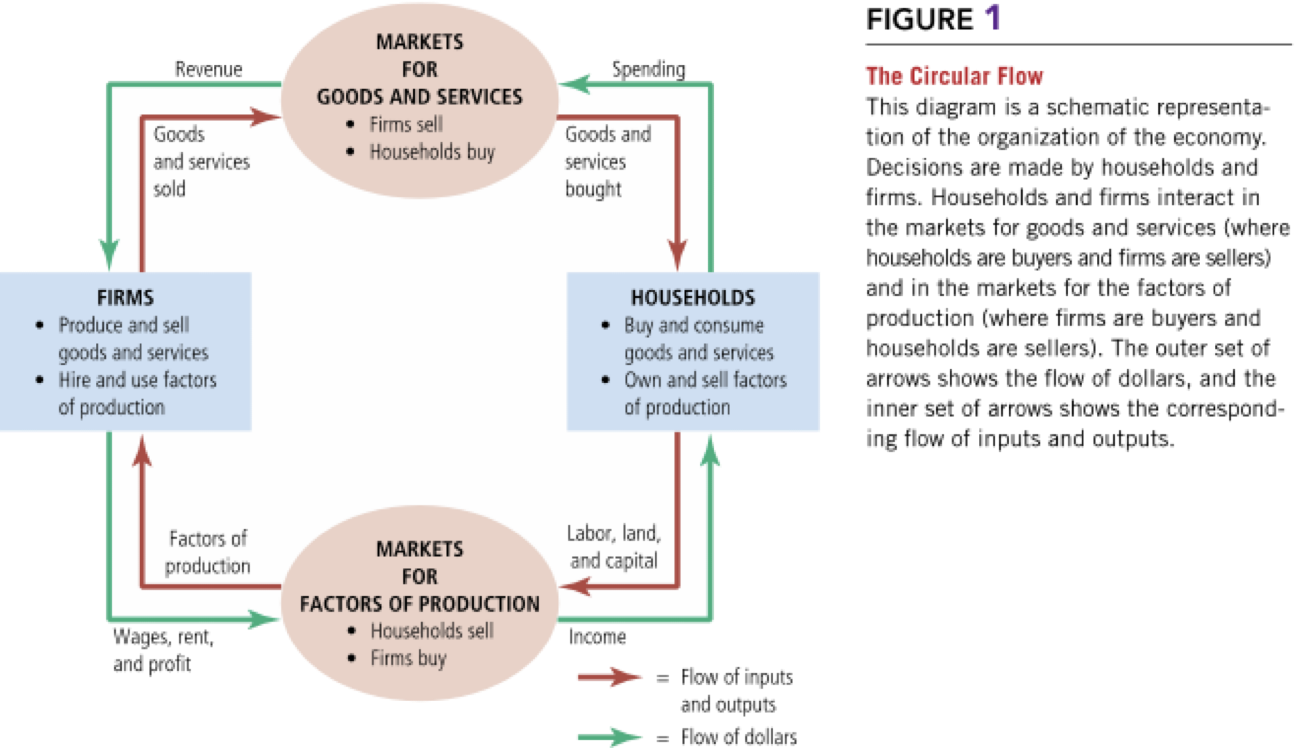

The Circular-Flow Diagram

- Visual model of the economy

- Shows how dollars flow through markets among households and firms

- Two decision makers:

- Households

- Firms

- Households

- Interact in two markets:

- Market for goods & services

- Market for factors of production

- Market for goods & services

The Circular-Flow Diagram

The Production Possibilities Frontier (PPF)

- Graph showing combinations of outputs an economy can produce

- Given:

- Available factors of production

- Available technology

- Available factors of production

The PPF - linear

The PPF - bowed outwards (increasing OC)

Areas of the PPF

- Efficient: points on the PPF

- Inefficient: points inside the PPF

- Not feasible: points outside the PPF

Microeconomics vs. Macroeconomics

- Microeconomics: decisions of households & firms; interaction in markets

- Macroeconomics: economy-wide phenomena (inflation, unemployment, growth)

The Economist as Policy Adviser

- Economists as scientists: explain events (positive statements)

- Economists as advisers: recommend policies (normative statements)

Positive vs. Normative

- Positive statements: descriptive, testable

- “Minimum-wage laws cause unemployment.”

- “Minimum-wage laws cause unemployment.”

- Normative statements: prescriptive, value-based

- “The government should raise the minimum wage.”

Why Economists Disagree

- Conflicting theories

- Different value judgments

- Yet, many propositions most economists agree on

Propositions Economists Agree On

- Rent ceilings reduce housing availability (93%)

- Tariffs & quotas reduce welfare (93%)

- US should not restrict outsourcing (90%)

- Eliminate farm subsidies (85%)

- Eliminate sports franchise subsidies (85%)

- Cash > in-kind transfers (84%)

- Large deficits harm economy (83%)

- Don’t ban GM crops (82%)

- Minimum wage increases unemployment (79%)

- Reduce ethanol subsidies (78%)

Summary

- Economists as scientists → assumptions & models (e.g., PPF, circular flow)

- Micro = individual decision-making; Macro = whole economy

- Positive = descriptive, Normative = prescriptive

- Economists may disagree (judgments, values)

- Policymakers may ignore advice due to politics